The graph illustrates this point for Australia (where the low point was in 1997-98) but, like asset inflation, this is also a global phenomenon.

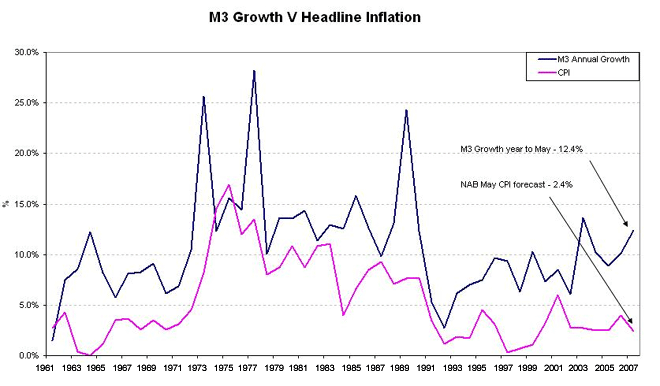

The graph shows the generally positive correlation between inflation and monetary growth. The correlation has been complicated by financial deregulation and involves fierce debate about causation - is money the horse or the cart?

Advertisement

This point is irrelevant to the conclusion that the rise in monetary growth - also a global trend - is a second sign of rising inflationary pressure. A third indicator is the rise of bond yields. The rise since 2003 has been in fits and starts but during June there was a decisive breakout in which yields on 10-year bonds in the US hit 5.3 per cent. There has been some retracement since, but like the rise of inflation itself, and the rise in monetary growth, the global trend in bond yields is now clearly established.

Sharp increases in commodity prices have also been part of the global inflationary trend, as a direct and much-commented-on influence of the BRICs-boom. Oil is one commodity whose influence cannot be ignored because of its influence on the price of petrol in the Western nations. Ominously, the price of oil is again trending up.

It's been the practice of central banks to downplay the price of petrol and other "one-off" sources of inflation as not part of so-called "underlying" inflation. But there is another emerging debate, reported last month by The Economist magazine, on the perils of this approach.

The Economist commented: "After a jittery few weeks, bond markets rallied on June 15th on news that the US's core consumer price index rose by just 0.1 per cent in May. The data was warmly greeted by stock markets too. The Dow Jones index rose by 86 points on the day. Investors decided that the absence of price pressures would calm the nerves of rate-setters at the Federal Reserve, who have been worrying out loud about "elevated" core inflation.

"What the markets blithely ignored was the day's bad news. Headline consumer prices rose by 0.7 per cent, the biggest monthly increase for nearly two years. Unlike core inflation, the headline measure includes fuel costs, which rose sharply, as well as food prices. For bond prices to rise on such a big jump in inflation, markets must be placing a great deal of faith in the core index as the true gauge of price pressures. Is that wise?"

Hear, hear, says Henry. Asset inflation is a wonderful thing for owners of assets, like Henry and readers of this newspaper. Sharply rising asset prices should nevertheless have produced tighter monetary policy sooner. This point is still controversial.

Advertisement

What is not controversial is that goods and services inflation, the currently conventional indicator of the need for policy action, is clearly on the rise. The RBA cannot act on its own, but the BIS report shows that the global central bankers are on the case. Action now would be politically awkward in Australia. Putting politics aside, as Glenn Stevens is duty-bound to do, better a 25-basis point hike now than bigger hikes in early 2008.

Over to you, Mr Governor.

First published in The Australian on July 3, 2007 and on Henry Thornton’s website.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

7 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon