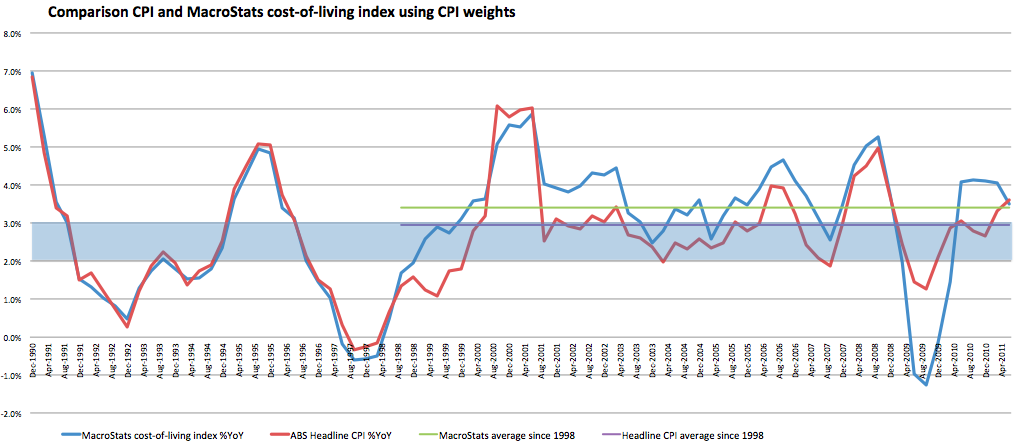

Using this data the cost-of-living index is about 0.5 percentage points higher on average since 1998.

So what led to the current mysterious situation surrounding housing treatment in cost-of-living indexes, and the complete removal of land from the CPI?

Advertisement

In 1997 the RBA argued strongly to remove the price of land from the CPI in its submission to the 13th Series CPI review. The RBA argued that including a mortgage interest component in the CPI would result in an inflation measure that is amplified by monetary policy responses to inflation itself. They say -

At a time when inflationary pressures are increasing, interest rates are being increased to combat those pressures. The interest components of the CPI also rise, adding a short-term impulse to inflation as measured by the headline (or total) CPI.

That is a reasonable argument in my mind. But their logic for me breaks down a little when they say that the acquisition of a house is really an investment activity, rather than consumption.

So why include it at all? Why not use an imputed rent for owner-occupiers to be consistent? Or use mortgage interest as a proxy for the annual benefits flowing from owner-occupied housing? Simply excluding land purchase costs without any proxy for the annual use of land is totally inconsistent.

To me you need to choose one treatment or the other. Either add the full cost of home ownership as a lump sum, either in the form of house prices, or add the cost as a periodic payment by the home-owning household to itself in the form of imputed rents. The RBA canvasses this approach in its submission but noted that this may cause a ‘disproportionately large’ weight to the housing basket.

The weight to be assigned to the Housing group would need to be adjusted to recognise that all owner-occupier households are paying ‘imputed’ rents to themselves, resulting in a disproportionately large weight on housing in the CPI.

Advertisement

The RBA submission mentions a number of times that they see a high weight on housing in the CPI basket as unfavourable. For example they note that by excluding the land component of house purchases the weight on housing would be substantially reduced. By international standards our basket weight to housing is low at 16.43%. Germany has a 20.33% weighting for rents alone (and another 1.4% for home maintenance), the US has 30% allocated to rents and owner-occupied imputed rents, the UK has housing at 20.9% and the Netherlands at 23%.

This is all very odd since the weighting of housing in the CPI is a key determinant of the CPI itself. The ABS noted this issue in their 2006 analysis, showing that the full weight of household expenditure on owner-occupier user costs was around 15.8% in 2003, yet the CPI measure allocated just 7.1% to owner-occupied housing costs.

Most interesting of all is that the RBA concludes in their submission that excluding interest charges would in no way distort the outcome over the long run. Well, I’m not sure just how long the long run was in the minds of the RBA staff at the time, but they probably weren’t thinking about periods longer than a decade. The mortgage interest charge line in the third graph above may very well return to the level of the current house purchase cost line. But as you can see, for this RBA assertion to hold true, home prices or interest rates need to fall quite a way.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

7 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon