What I want to talk about today is the pause that Biden enacted on the leasing of gas and oil leases on public land at the beginning of the year, why he did it and what the price effect of that is on West Texas Intermediate Grade oil. In doing so I'm using a framework that was invented by the man who pretty much began the economics of climate change in the United States. That man is William Nordhaus.

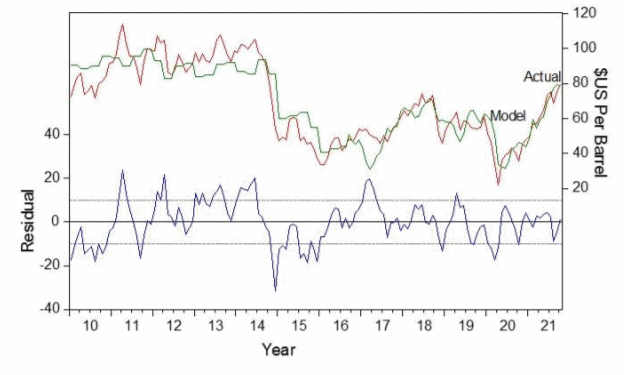

Figure 1 : Model of US West Texas Intermediate Grade Oil Price

Source: Morgans

Advertisement

Nordhaus was a macro economist from the 1960s, he was part of the group of economic advisors in the Carter presidency in the 1970s. He started writing seriously about climate change in the 1990s. He was president of the American Economic Association in 014-2015. First time I ever saw him present in person was in 2015. He has a great way of calming a room and bringing together disparate forces to a civil discussion. He won the Nobel prize for economics in 2018 because of his work in climate change. It was Nordhaus that invented the carbon tax. What he was doing was attempting to model a relationship between an increase in the prices of carbon and decreasing the use of fossil fuel and the decreasing production of CO2.

The problem was in the United States even though there has been a large number of attempts to introduce a carbon tax, none of them were politically successful because no politician wanted to be seen to put up prices for consumers. When Biden came to office what he decided instead of moving the price, he would just move the quantity. He would reduce the quantity of oil and gas being produced in the United States by "pausing" the provision of oil and gas leases on public land.

The way we measure the effect of this is similar to the way the RBA measured the announcement effect of quantitative easing in a piece they published a couple of months ago. We put in the dummy variable in the series for the event and we measure what the effect of that event was on the price of West Texas Intermediate Grade. We start, as we usually do, with our model of West Texas Intermediate Grade which is constructed in the conventional way.

In our model, the price of West Texas Intermediate Grade is determined by those stocks levels that you see announced every week by the Energy Information Authority (EIA). When you put those into a model based on the last 10 years of data what you find is the relationship between those stock levels and the West Texas intermediate grade price is incredibly powerful. The "T" statistic is 24. This means that the chance of this being a random relationship is vanishingly small.

In addition, we put in a dummy variable not for politicians but for the policy action beginning in February this year. We measured the impact of that statistically, and what we find is the model explains a bit over 80% of monthly variation in West Texas intermediate grade. Our model is shown in Figure 1. The effect of the announcement of the pause in oil and gas leases on public land increases the West Texas intermediate price by $13.34. It adds $13 to the price now.

This price seems to be increasing over time. As we go further into the future there's less and less gas and oil available to the market, so over an extended period this might wind up to be another number, a higher number. Right now, the "T" statistic of the data is 3.8. This means the chance of this relationship being a random event is two chances in ten thousand. What in fact has happened is that Biden's brought about a price effect in response to reducing the quantity of oil and gas leases available to the domestic market.

What's that supposed to do? If we go back to Nordhaus, the "pause" makes it more and more economic for other forms of energy to be produced, other forms of energy which are less carbon intensive. In that circumstance doing things like imposing a ban on the US export of oil or to begin selling down the US strategic oil reserve would be self-defeating in terms of the policy response that the pause in oil and gas leases was attempting to produce.

Advertisement

Still, this is a very good thing for oil and gas producers in the rest of the world. The fact is that the United States is attempting to force up the oil and gas price. This is something that can be harvested as a benefit both by Australian oil and gas producers and certainly by the OPEC Cartel.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

4 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon