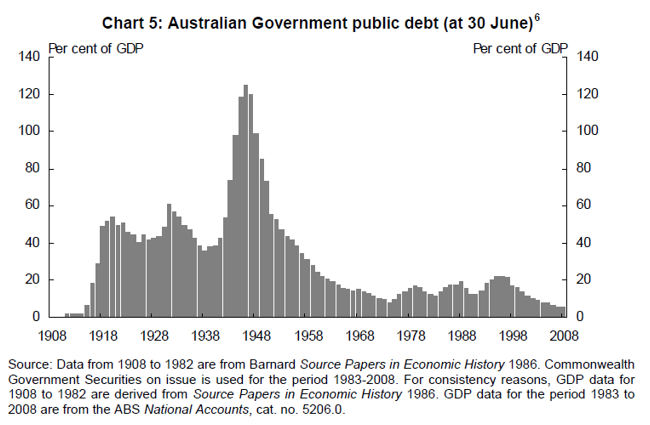

Most people understand Quantitative Easing as unconventional monetary policy. Still, for most of Australian history, after the second World War, it was extremely conventional monetary policy. In 1946, at the end of WWII, Australia had a gross sovereign debt of a little over 120% of GDP. That was as a result of the debt from both World Wars. The problem was how to pay it back. The way to pay it back was to run continual budget surpluses. The Menzies government from the beginning of its second term up until the end of the governments that succeeded it in 1972, ran at a continual surplus. By the time we reached 1974 the gross sovereign debt had fallen to 8% of GDP.

Figure 1: A history of public debt in Australia

Advertisement

That wasn't all of the problem, the problem was that you needed to sustain a moderate level of inflation at the same time. The literature would suggest that Menzies wanted to target an inflation rate of about 4%. There's a record of him talking about this, when he's on the campaign trail, for his second term in 1951. How could Menzies continually run budget surpluses, to pay back the national debt, while maintaining an inflation target of 4%? In the end, they managed to achieve an inflation level averaging 3.7% for the period, from January 1952 to December 1972. So, how was it done?

Back in the day, when I began to study economics, we learnt that one of the common ways of financing government expenditure, was to sell debt to the Central Bank. In other words, what today is considered unconventional, was extremely conventional. By continuously selling a proportion of the sovereign debt, as it was rolling over for refinancing, to the Central Bank, we could generate growth in the money base which would generate growth in the money supply. This generated lending and managed to maintain inflation around 3-4%.

This process of rolling over a proportion of debt while running a budget surplus, has been demonstrated in Australian history as a successful way of managing a healthy growing economy.

This conventional monetary policy only became unconventional in around 1982-1983. At that time, there was an agreement between Treasury and the RBA to stop financing Commonwealth debt, by selling it to the RBA. They did that because they needed to generate a series of conditions to launch a floating AUD. It was thought that if they continued financing Commonwealth debt by selling it to the RBA, this would generate the expectation of an unstable foreign currency.

What the RBA expects

If we look at the outlook that has been provided with the Quarterly Statement on Monetary Policy, the RBA does not think that the Australian economy is going to go into recession. The RBA thinks that inflation is far too low and will be sustained at a level far below its inflation target.

Advertisement

The Quarterly Statement Outlook, released on 8 November 2019, suggests that GDP growth this year will be 2.3% with CPI of 1.8%. It also suggests, that growth next year will be 2.8% with CPI at 1.8%. It suggests that the year after, growth will be 3%. All of these are good numbers, but inflation is still only 2%. (Over the RBA forecasting horizon, inflation remains below the target range of 2.0% - 3.0%). The major issue for the RBA here is not growth, it's getting inflation up to the inflation target.

What the Governor has said

Speaking at the Australian Business Economists dinner in Sydney, on 26 November 2019, the RBA governor Philip Lowe, said "if the Reserve bank were to undertake a program of QE, we would purchase government bonds, and we would do so in the secondary market. An important advantage in buying government bonds over other assets, is that the risk-free interest rate affects all asset prices and interest rates in the economy. It gets into all the corners of the financial system, unlike interventions in just one specific private asset market".

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

4 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon