It would be astounding if the Reserve Bank did not cut Australia's cash rate today, possibly or probably by another 100 basis points.

Most recently, the International Monetary Fund has been embarrassed by its fourth or fifth downward adjustment to its predictions about global growth. Now the IMF suggests global growth will be close to zero in 2009 and not much better in 2010.

At Davos, politicians, businessmen and analysts exhibited deep gloom. Anatole Kaletsky of The Times suggested last week that the views of such "opinion leaders" are a contrary indicator, and their gloom should be our cheer. Certainly, this time last year, the great and the good at Davos were relatively cheery, their optimism clearly contradicted by events in the past year.

Advertisement

Governments everywhere are discussing, or implementing "stimulus" packages of fiscal expansion. Economic theory calls only for fiscal stimulus when monetary stimulus fails, like "pushing on a string", as Keynes said.

I doubt that Australia needs much fiscal stimulus, except that which improves national productivity and competitiveness.

Handouts to battlers, spending on infrastructure, physical infrastructure like railroads and ports, or "enabling" infrastructure, such as spending on R&D and education, and tax cuts all have been implemented or are under active consideration. All actions of this type have their pros and cons, but too much should not be expected. Temporary "sugar hits" in battler bailout may be saved (or gambled away) and no budget can afford too many handouts.

Infrastructure spending takes time to organise and may come on stream just as other forms of spending is cranking up. Tax cuts appeal most to deep-dyed conservatives, as they leave decisions to spend or to save in the hands of those who earn the money.

Global fiscal policy will influence the global tide of economic activity, but winners and losers will be decided in part by policy actions in each nation. Fiscal actions that increase Australia's productivity and competitiveness are the most sensible option, as they will improve Australia's position when recovery comes.

National leaders and the international agencies are saying the right things about the avoidance of a slide into protectionism. But industrial bailout - of banks, motor vehicle manufacturers or property developers - is a form of protectionism.

Advertisement

The major banks are so important to the global economic system that they cannot be allowed to fail. But allowing failed bankers to walk away with bonuses that in aggregate add up to tens of billions of dollars is at best unpalatable, and in any case is morally unacceptable. Allowing bank shareholders to escape with their capital augmented by taxpayer's funds is also morally unacceptable. Henry has no problems with part-nationalisation or even full nationalisation of banks that need to be bailed out by capital injection of taxpayers' funds. Such an approach gives taxpayers a chance of eventually recovering the money used for the bailout. However, it must be stressed that companies requiring injection of fresh capital should first go to the market.

Companies requiring new capital would naturally investigate merger, sale of equity to investors, including in cashed-up nations such as China or wealthy nations in the Middle East, or put themselves in the hands of administrators to arrange an orderly wind-up. These are all alternatives for boards of directors unable to swallow the deal a government might offer.

Governments demanding tough terms for corporate bailouts would encourage rapid adjustment in the capitalist system and the net effect might be rapid reconstitution of failed enterprises under new management and the further encouragement of capitalism in nations not currently strong bastions of free enterprise.

An objection might be that governments would be unable to find people able to run failed banks, vehicle companies or property developments. I suggest this would be the least of governments' problems, as there are many competent older people who would welcome the chance to earn a modest salary (perhaps also a modest bonus for stellar performance) in return for reintroducing conservative old-fashioned management practices in newly or part-nationalised companies.

There is a point specific to the Australian banking sector. Much is made of the relatively sound position of Australia's banks. The truth is that they funded housing loans with overseas borrowing. When the global credit markets froze, Australia's banks were in real trouble. They were bailed out by the government lending them its AAA rating.

If a wealthy entrepreneur had provided the bailout (as Kerry Packer did for Westpac in the previous crisis) he would have taken a large slice of equity in return. Why should Australia's taxpayers not get equity for the bank bailout in this crisis?

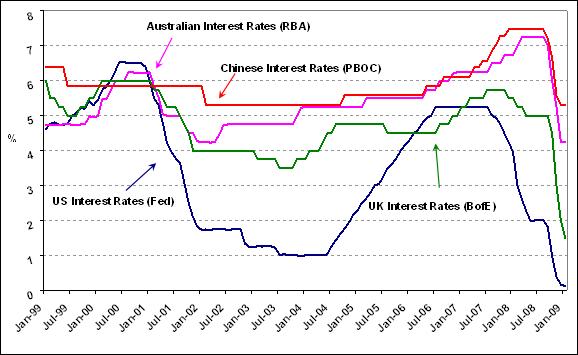

I return now to a discussion of monetary policy. Henry has for several years said that US cash rates were too low in the early years of this century, and this view has gradually become more widespread. The result of US cash rates at 1 per cent in 2003-04 was a series of asset bubbles and the build-up of consumer inflation globally.

Now US cash rates are again close to zero, and the US Fed is again flooding the world economy with liquidity. It will be impossible to withdraw liquidity when global recovery gets under way, and there will be another bout of asset inflation, leading inexorably to consumer inflation and eventual monetary tightening too little too late, overshooting and another episode of global slowdown.

Other nations cannot avoid this stop-start instability. In theory, a flexible exchange rate enables any particular nation to avoid being carried along for the ride, and this is especially the case when the most important global currency - the US dollar - is generating the global instability.

The growth of money and credit in Australia has declined substantially. But liabilities of the Reserve Bank have exploded in the past quarter to be an alarming 73 per cent above the level of 12 months ago. This deserves serious attention and explanation.

I have the following suggestions for Rudd and Swan and for the Reserve Bank's Glenn Stevens.

Rudd and Swan, by all means implement more fiscal expansion. The more you can focus on policies that boost productivity and contribute to Australia's competitiveness, the better it will be for our economy and therefore our battlers. This means policies that encourage households to save and to work, and that stimulate productivity.

Glenn Stevens, try to avoid too much easing of monetary policy. Australia can to some extent stand aloof from the rush to reduce interest rates to a point that makes another burst of inflation inevitable. You are best placed to judge that point, but your aim should be to facilitate real growth of, say, 4 per cent with inflation of 2 per cent. A modest undershoot of cash rates consistent with that growth is sensible now, but please remember the adjective.

And Henry implores Australia's powerbrokers to devise a fair and effective back-up system of corporate recapitalisation where market solutions fail and injection of taxpayers' funds is necessary to promote and preserve employment. In particular, there should be no taxpayer-funded corporate bailout without the government taking equity.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon