The potentially serious consequences of sustained high food prices were recently underlined by Robert Zoellick, president of the World Bank, who suggested that 100 million individuals could be pushed below the poverty line, thus wiping out seven years of gains against poverty.

There is however no agreement as to what explains the dramatic rise in food prices. One thing seems certain though: absent a global understanding between producer and consumer countries, current high prices could last for a long time.

Four basic drivers seem to stimulate rapid growth in demand for food commodities.

Advertisement

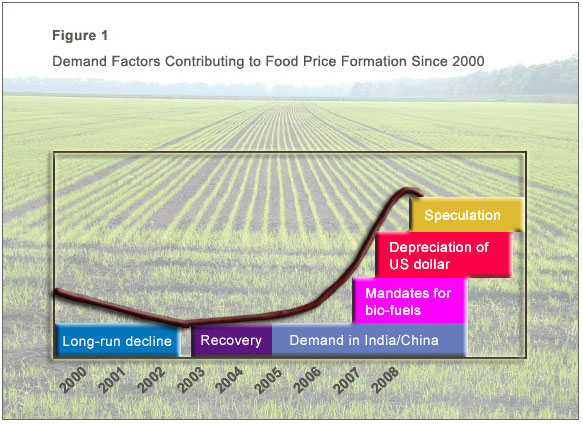

First, rising living standards in China, India and other rapidly growing developing countries, which lead to increased demand for livestock products and the feedstuffs to produce them. Second, stimulus from mandates for corn-based ethanol in the United States and the ripple effects beyond the corn economy that are stimulated by inter-commodity linkages. Third, the rapid depreciation of the US dollar against the euro and a number of other important currencies, which drives up prices of commodities priced in US dollars. And finally, massive speculation from new financial players searching for better returns than in stocks or real estate. Underneath all of these demand drivers is the high price of petroleum and other fossil fuels.

Figure 1 shows an impressionistic attribution of the four demand factors causing the recent run-up in food commodity prices. The figure also shows the recent component of the “normal” long-run decline in food prices that has been experienced over the past two centuries or so and a modest recovery from the lows reached in the early part of this century. However, the surge in food prices that has attracted so much attention did not start until 2005 or so, depending on the commodity. Substantial speculative investments in food commodities seem to have started only in mid-2007.

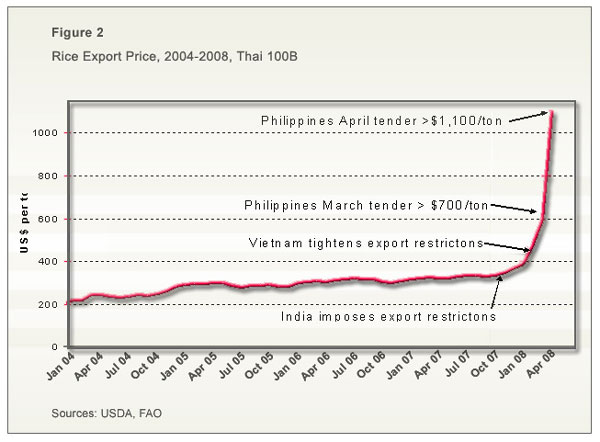

Each of the four demand-driven causes differs slightly for each basic commodity, but the underlying forces are similar. For rice, however, the story is more complicated, as seen in Figure 2. The actual production/consumption balance for rice is favourable. The problem is that a few importing countries, the Philippines in particular, are trying to build up their stocks to protect themselves against shortages going forwards.

Of course, if every country or individual consumer acts the same way, the hoarding causes a panic and shortages, leading to rapidly rising prices. Even US consumers are not immune from this panic.

Advertisement

Such price panics have been fairly common during the past 50 years, but the hope was that deeper markets, more open trading regimes and wealthier consumers that could adjust to price changes had contributed to market stability. This was wishful thinking, as it turns out, as the recent price record for rice shows.

For some food commodities, especially wheat, drought and disease have also led to significant supply shocks. Normally these would cause only modest increases in price, with supplies from stocks and a pattern of year-round production in the northern and southern hemispheres dampening upwards movements. But wheat stocks were at historic lows even before the bad crops rippled around the world in 2007, and the spike in wheat prices has been dramatic. The recovery of Australia’s wheat crop, currently being harvested, has caused a significant decline in wheat prices since early April.

Inter-commodity linkages triggered the current spike in rice prices. In India, as in other parts of the world, drought and disease damaged the 2007 wheat harvest. Thus the national food authority had less wheat for public distribution. Importing as much wheat as in 2006 - more than 7 million metric tons - would be too expensive because of the high prices in world markets. So the food authority announced it needed more rice from domestic production.

India - the second largest rice exporter in the world, with 5 million metric tons last year - put barriers on rice exports, and other rice exporting countries followed suit, as rice prices started to spike.

The newly elected populist government in Thailand did not want consumer prices for rice to go up, and the commerce minister openly discussed export restrictions from Thailand - the world's largest rice exporter, with 9.5 million metric tons last year. On March 28 rice prices in Thailand jumped $75 per metric ton.

Since then, prices have continued to skyrocket and now, when rice is available at all, it costs more $1,100 per metric ton. This is the stuff of panics.

Rice stocks in Asia have come down over the past decade, but that was a sensible response to growing reliance on trade as the buffer. Holding rice stocks in tropical conditions is extraordinarily expensive, so a smoother flow of rice internationally reduces wasteful stockholding. Now that the exporting countries put bans on rice exports, nearly all countries will be forced to resort to domestic stockpiles. That is a real tragedy for poor consumers and for economic growth.

The most volatile element in the food commodity boom is the “hot money” in search of the next investment boom after the crash in tech stocks followed by real-estate derivatives. The real trigger for the current spike in food prices is speculative behaviour on the part of large investment/hedge funds with hundreds of billions of dollars looking for the next price bubble.

The combination of a rapidly falling dollar, movement of investment funds into commodities, especially petroleum, and then out to other commodities is the trigger needed for the food market to explode. The Bank of International Settlements in Basel estimates that hundreds of billions of dollars are now invested in commodity funds.

The need for changes in trade policy in the world rice market is clear. With India, Thailand and Vietnam - the three largest exporters to the world rice market - all more-or-less withdrawn from the market, and importers such as the Philippines and a number of countries in Africa increasingly desperate to lock in supplies, there is a need for a high-level forum to get all countries to agree to keep their borders open to rice imports and exports, even in times of crisis. Otherwise we have a 1930s-style depression with "beggar my neighbour" policies causing each economy to spiral downwards.

The longer-run question is whether supply dynamics will begin to match the rapid growth in demand. In past episodes of high food prices and fears of Malthusian crises, supply responses have been vigorous, albeit with a lag, returning world food prices to their long-run downward trend. This time, arguments increasingly suggest that there is little supply response left in the system, for three basic reasons:

- there is little high-quality agricultural land to be opened;

- the yield potential of existing agricultural technologies has been static for decades: closing the gap between this yield ceiling and actual farmer practices is the only source of increased output, and this gap has been closing rapidly everywhere except Africa; and

- the costs of inputs needed to achieve higher yields are high and rising, especially for fuel, fertiliser and water.

Unless major exporters and importing countries can arrive at an agreement to cool the hoarding and speculative binge, the prospect is that high food prices, perhaps near current levels, will be a market reality for many years.

Reprinted with permission from YaleGlobal Online - www.yaleglobal.yale.edu - (c) 2008 Yale Center for the Study of Globalization.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon