In the debate over oil supplies, July 2007 may be seen as a turning point. The International Energy Agency, a body set up to advise OECD nations on energy supply and security, broke with its previous optimistic projections of world oil supply and threw the future of oil into doubt. The IEA’s recently released “Medium-Term Oil Market Report” (PDF 1.87MB) reads like a summary of peak oil concerns made acceptable for the ears of government by occasional disclaimers to the contrary. However, its central declaration is clear:

Despite four years of high oil prices, this report sees increasing market tightness beyond 2010, with OPEC spare capacity declining to minimal levels by 2012 … It is possible that the supply crunch could be deferred [by decreased demand growth] - but not by much.

Advertisement

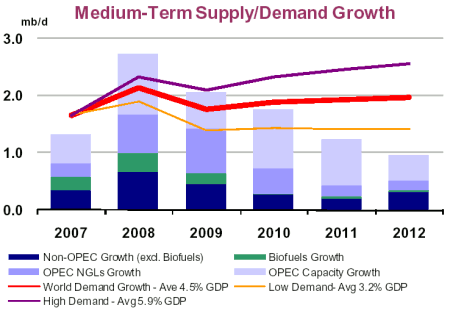

As the chart above indicates, even if growth in demand is lower that expected, growth in oil supply nevertheless fails to meet growth in projected demand by 2011. If world demand growth is higher, then the oil shortages come sooner.

The chart above also shows a number of other interesting points. While considerable new supply should come on stream in 2008 (and lead to a temporary drop in fuel prices) there is less optimism for later years. Also, the growth of biofuels, while significant, is relatively limited. (When examining the chart, remember the world is currently using about 85 million barrels of oil per day [mb/d].)

It has been the habit of previous Medium Term Reports to assume that the OPEC nations will raise production to meet any shortfall in growth from non-OPEC suppliers. However, now this report declares:

Recent history would suggest that a conservative approach to OPEC capacity is justified.

Despite the declaration of caution, the IEA then makes assumptions of Saudi Arabian capacity that are not justified by its production performance over the past few years, including recent times when oil prices have been high and would reward maximal production.

As illustrated by an insightful comment on the website, www.theoildrum.com, the IEA assumes current Saudi capacity that is probably over 1mb/d greater than reality. Saudi Arabia’s declared ability to increase production is very important in the IEA’s growth projections for the next five years but in the contrarian peak-oil community there is considerable debate over the truth behind Saudi Arabia’s claims.

Advertisement

The IEA report is also quite upbeat about new refinery capacity coming online, especially in the Middle East and China, and the effects this will have on fuel availability - at least for everything other than shipping (see below). As the world’s easily extracted oil comes to an end, the "heavier" (more viscous), more "sour" (higher sulfur) grades remain. This oil requires greater processing by refineries before it can be used but world refinery capacity has recently be struggling to cope with demand due to decades of underinvestment. However, that is now changing:

The refining industry … has responded to market incentives. Investment in sophisticated refinery capacity is continuing apace … a significant improvement in refinery flexibility is foreseen.

Interestingly however, this increased refinery capacity shows that every silver-lined cloud has a black interior. At the moment, shipping uses heavy grade fuel oil that is cheaper than the lighter grades of oil more suited to gasoline and diesel fuel production. However, if the capacity exists to refine heavier oil grades into gasoline then:

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

38 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon