On Line Opinion is a not-for-profit publication and relies on the

generosity of its sponsors, editors and contributors. If you would

like to help, contact us.

___________

There is no way the truth about these injuries can be permanently suppressed.

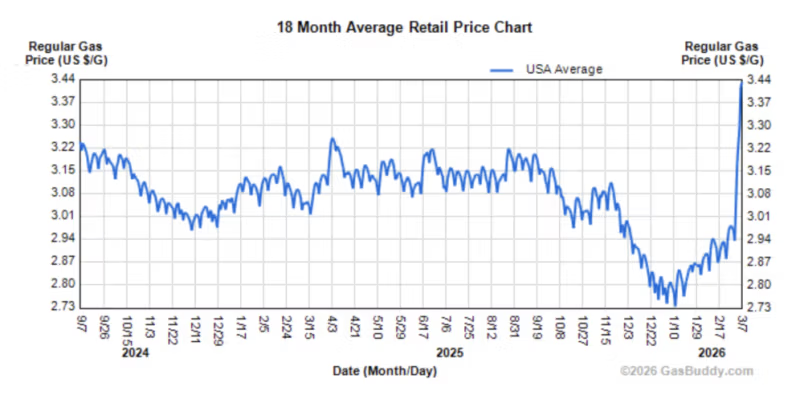

The higher gas prices are in the news and the obvious culprit is the war on Iran which has disturbed shipments through the Strait of Hormuz. But there is another factor here rarely mentioned. Refining capacity in the US never recovered from lockdowns. Before, the previous peak was 19M barrels per calendar day. That dropped in 2021 to 18.1M and further to 17.9M in 2022. We are still 0.5-0.6 million below the pre-lockdown peak, meaning that any disruption was destined to have a big effect on oil prices and prices at the pump.

Advertisement

That disruption came with the Iran war. As for the Strategic Petroleum Reserve, that was already tapped out during the last lockdown-driven and inflation-induced price spike. The low prices of 2025 could not last with any stress on production structures.

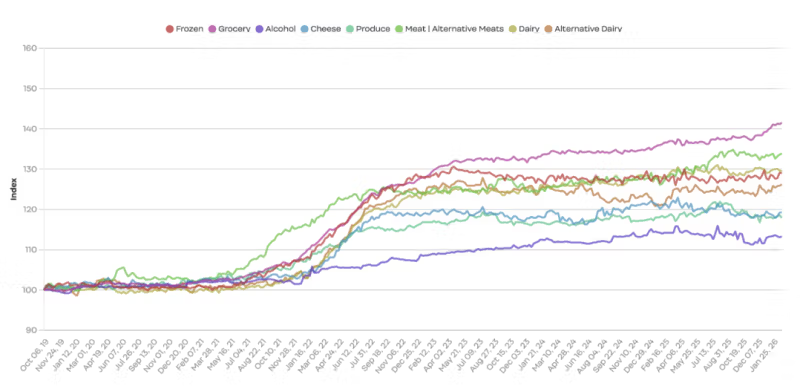

And speaking of inflation, that lockdown-triggered money flood from 2020-2023 ended up taking a 30-40% bite out of the dollar’s purchasing power, causing a flattening of wages and salaries in real terms, even as housing prices skyrocketed far beyond middle-class affordability. Groceries never came back to being affordable again.

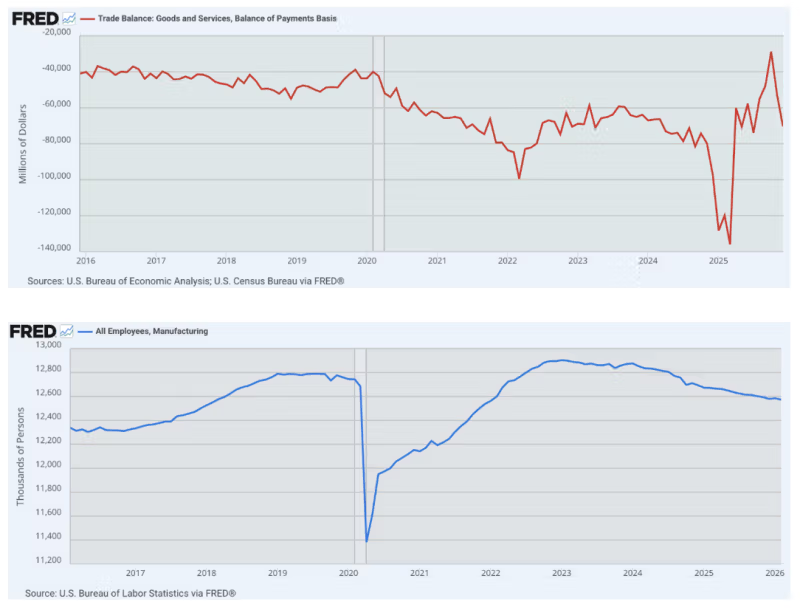

Manufacturing was devastated during the Covid years with global supply-chain disruptions. Trump came to office a second time determined to fix this but chose the blunt instrument of tariffs which are higher now than in a century. The effect of these has not been to lower the trade deficit but rather increase it (the opposite of what was supposed to happen), even as manufacturing employment continues to fall.

Advertisement

At this point, there is no evidence that this strategy has worked in any sense, except to raise money for the federal government and provoke a Supreme Court decision that essentially restates what is already in the US Constitution. One wishes the Court would do that more often.

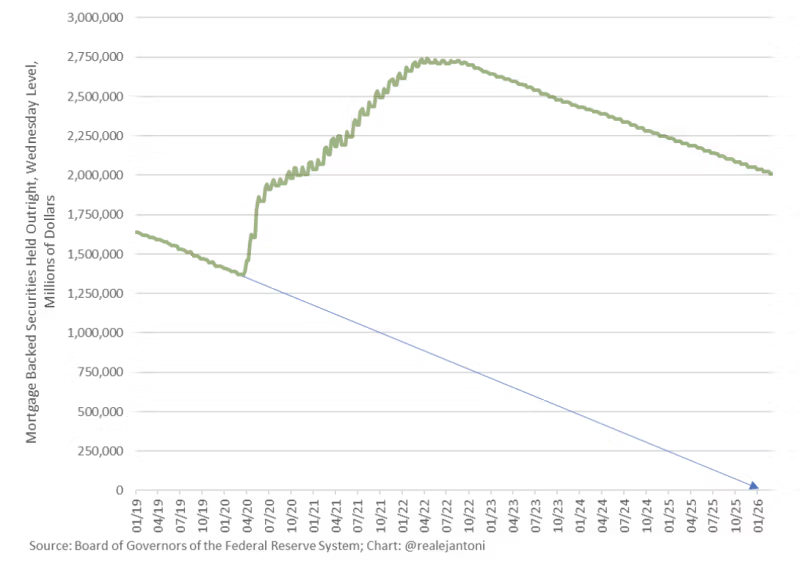

Back to the Federal Reserve, EJ Antoni documents how the Fed was working to fix its balance sheet before the quantitative easing of the Covid years. It was on track to offload all its mortgage-backed security products but that progress was interrupted. Even now, the Fed’s balance sheet is a disaster to the point that the Fed is paying out $300 million in interest daily, mostly to foreign financial firms and central banks.

Jeffrey Tucker is Founder, Author, and President at Brownstone Institute. He is also Senior Economics Columnist for Epoch Times, author of 10 books, including Life After Lockdown, and many thousands of articles in the scholarly and popular press. He speaks widely on topics of economics, technology, social philosophy, and culture.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon