I want to talk purely about the effects on two particularly important markets – oil and wheat – and how they have been affected by the conflict in Ukraine.

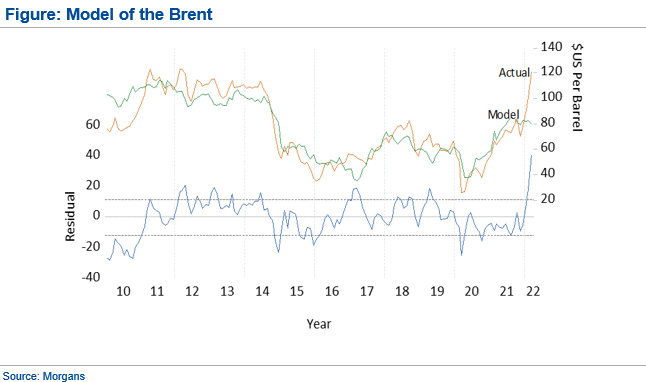

Saudi Arabia is the world's largest exporter of oil, but the second largest is Russia. How do we model Russia in terms of its impact upon markets? Shown below is my updated model of the Brent price. What you can see in that model is the equilibrium price of Brent based on the level of stocks of product plus currency effect. This explains 80% of monthly variation of the Brent Oil Price. It tells us the equilibrium Brent Oil Price should be $80 a barrel. The West Texas model estimate is about $2 less than that. Still, the oil price is much higher. The price of Brent is about US$109 per barrel and the price of West Texas is only slightly lower than that.

So how do you account for the difference between the model of the oil price based on fundamentals, stocks, and currency effects - which explains what happens most of the time - and why the price is so much higher than that? The difference between the two is war risk, and I want to define war risk in simpler terms.

Advertisement

What has been happening over the past month, as we know, is that Russia has been subject to new sanctions and that has affected important things like the ability of its central bank to operate. There has not been a central bank which has been subject to international sanctions in the way the Russian central bank has since Germany was subject to similar sanctions in the first World War. It is more than 100 years since sanctions this severe have been imposed. Still, what else has happened is something that has nothing to do with sanctions

.

It is perhaps an own goal of the Russians themselves. One of the time-honoured ways of running a naval campaign is blockade, making it impossible for ships to load at your opponent's ports and take away their exports. Well, the Russians seem to have done this to themselves by generating a situation where the war risk in the northern Baltic Sea is so high that it is almost impossible for ships to get insurance to enter the northern Black Sea and load either wheat or oil at Russian ports. So that means you cannot get cargos of Russian oil or Russian wheat loaded for export.

In contrast, the main reason Russian crude oil and refined product exports have been at risk since Russia's invasion has been the refusal of financial institutions to back such transactions. In addition, oil tanker rates for Russian destinations rose to record levels, reflecting public pressure on oil companies to avoid purchasing Russian oil, fear of official sanctions on Russian energy exports at a later date and attacks on vessels in the Black Sea. This outcome was unanticipated, as U.S. and European Union sanctions originally deliberately excluded Russian energy exports.

Additionally, financial institutions are refusing to back such transactions. And what that means is suddenly one of the world's largest exporters in both of those markets disappears. That is how you define war risk, and that is why the price is so much higher. This is something the Russians have done to themselves, and it is this effective embargo on themselves that has driven the price up.

Advertisement

We know about oil, and everybody has been talking about oil, but I want to also reflect upon the effect of what this is doing in the world wheat market. Russia is the world's largest exporter of wheat. It exports 37 million tonnes every year. The US is the second biggest exporter of wheat. It exports 26 million tonnes every year. Ukraine, very interestingly, is the fifth largest player exporting 18 million tonnes every year and Australia is normally next. Our exports actually rose in 2021 to 25.5 million tonnes. The fact is there is this huge lift in the wheat price. Our equilibrium model for the wheat price is based on the level of stocks that are expected to be available.

The model has currency effects in it as well. Currently our wheat price model is running at US$8.14 a bushel. This is the highest level that the model has ever been in the many, many years that we have been running this model. Still, the actual price is $11 a bushel, $3 a bushel higher than that or some 35% higher than the model equilibrium price. That is because the ability to load cargos of Russian grain and Ukrainian grain is made impossible because of war risk, because ships cannot insure themselves to load at those Black Sea ports to take those cargos.

The effect of the Russian invasion is not limited to energy markets. Russia and Ukraine together account for 29% of global wheat exports. The disruption of exports from the Black Sea together with financial sanctions on Russia means the supply of wheat and other grains is likely to be curtailed in 2022 and beyond. The diminished supply, along with a shortage of fertiliser produced from natural gas, will drive up global food prices and reinforce the growth-retarding and inflationary effects of higher fuel prices. Likewise, the war is driving up the price of raw materials and metals produced in Russia.

Now, why this is important outside both of those countries and outside Australia is that we had an event quite similar, but not identical to this, in 2008 when we had the current low level of world stocks of wheat. At that time, we had an overshoot in the price. At that time the overshoot in the price generated world food riots throughout the under-developed world. The riots were particularly bad in Egypt, Pakistan and in other developing countries.

This problem, I expect, is going to repeat itself over the coming months. The wheat price will overshoot, stay high and that could generate shock waves and food riots around the developing world.

It is not normal fundamentals that are driving these prices higher. It is war risk - the inability of ships to load cargos of either Russian oil, Russian wheat or Ukrainian wheat at north Black Sea ports. That problem will continue for as long as this war continues. This is a pretty good reason for Vladimir Putin to think about stopping this conflict as soon as he can.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon