Everything we do before a pandemic will seem alarmist. Everything we do after will seem inadequate. Michael Leavitt

Summary

In response to widespread concern regarding the intensity and duration of economic impacts from the current COVID-19 pandemic, this article aims to inform discussion by (1) identifying the mechanism through which shocks to individual markets are transmitted to the aggregate economy (2) providing plausible upper and lower bounds for impacts drawn from actual economic data for most recent pandemics, and (3) estimating the magnitude of government intervention required to counteract the economic impact of the pandemic. The key finding is that the impact of COVID-19 on Australia’s economy is likely to be deep - a contraction of up to 15 percent of GDP - and require government expenditure of at least $300 billion billion to offset the shocks to the labour market, consumption and investment.

Advertisement

Introduction

In economic theory, the output of the aggregate economy (Y) is composed by the sum of private consumption (C), government expenditure (G), business investment (I) and exports (X) minus imports (M); and is conventionally stated as Y = C+G+I+X-M. The equilibrium growth path of the aggregate economy, therefore, can be understood as the sum of the growth paths of its components. The Australian Bureau of Statistics (2020) estimates the annualised output of the Australian economy (Y) in the December 2019 quarter had a value of almost $2 trillion, composed of $1.1 trillion in private consumption (C); $700 billion in government expenditure (G); $120 billion in investment (I); $493 billion in exports (X); minus $425 billion in imports (M).

The introduction of an external shock to one or more of these sectors will require offsetting change in others to restore the equilibrium of the aggregate economy, that is, the path of output along which supply balances demand. Otherwise, the risk of a recession is run. This is precisely the situation unfolding in Australia as significant decline in household consumption, business investment and exports requires counterbalancing by government expenditure to restore the economy to equilibrium.

The economic transmission mechanism

The specific transmission mechanism through which economic shocks from COVID-19 to individual markets flow to the aggregate economy can be described as follows. First, a reduction in the short-run supply of labour in the market due to social isolation, illness and death leads to significant reduction in household consumption. Households reduce their consumption as they cannot travel, are concerned for their income and savings, and perceive their capital assets (primarily their home) to have declined in value. This is the well-known “wealth effect”. The most immediate detrimental economic impact is borne by the hospitality, leisure, travel and tourism sectors due to reduction in discretionary spending and the impact of social distancing rules. Reduced household consumption reduces business confidence and its willingness to invest and employ, deteriorating the employment outlook. Reduced household consumption, combined with reduced business investment and employment, impacts government tax revenue through the collection of less GST and personal and corporate income tax. Both exports and imports can be expected to decrease as demand from household consumption and business investment decline across many countries. The solution, therefore, to short circuiting this vicious spiral is to increase government expenditure to the extent required to offset the reductions in the other sectors.

At this time, fiscal policy is preferred over monetary policy as the policy lever of choice because official interest rates around the globe are at or close to zero and there is little room left for manoeuvre to stimulate aggregate demand through further rate reductions. In any event, cautious and debt-laden households are likely to repay debt rather than consume more. That said, the central banks’ practice of quantitative easing whereby they purchase financial instruments such as government bonds to maintain prices, liquidity and confidence will continue to assist in sustaining the economy.

Advertisement

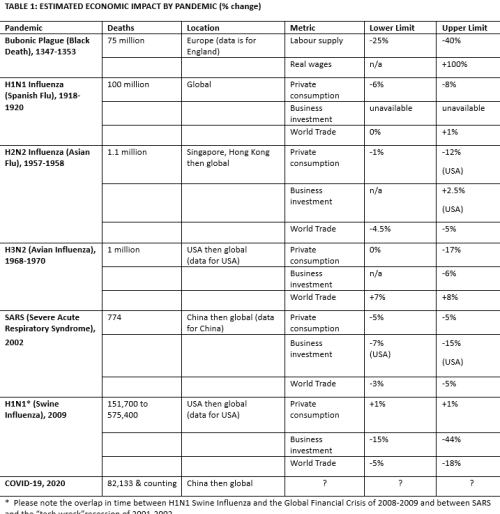

Data from recent pandemics

Table 1 summarises actual economic data drawn from five relatively recent pandemics to help identify plausible upper and lower bounds for key economic impacts. Data for the SARS pandemic of 2002 is included - despite the relatively small number of deaths - due to its similarity in geographic dispersion to COVID-19. Data for the bubonic plague, popularly known as the Black Death, which inflicted Europe between 1347 and 1353 is provided as a historical benchmark.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

7 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon