In this article, I'll talk about the outlook for the US economy that was released by the Federal Reserve in September. At this meeting the Fed cut the Fed funds rate by 25 basis points to an upper limit of 2%. The effective rate of Fed funds has actually fallen to 1.9%.

Fed repurchasing operations

I've been asked about Federal Reserve repurchasing operations. There was a sharp upmove in the price of funds in the repurchasing market on the 17th of September. As opposed to an effective target Fed funds rate of about 1.9%, the rate in that market on the 17th of September went to 5.25%. (All this is available on the Federal Reserve Economic Database (FRED). You can look it up as SOFR FRED (Secured Overnight Financing Rate).)

In response to that spike in the SOFR, the Fed repurchased US treasuries in the market. They did this to provide liquidity into the market and the banking sector. The amount of securities they purchased on 18th of September was $18.9 billion. As a result, the SOFR rate fell dramatically by the 23rd of September to 1.85%.

Advertisement

The result of that is the Fed reduced its repurchasing operation from $18.9 billion on the 18th of September to $100 million on the 24th of September. They entirely dealt with the problem. This really wasn't actually a big financing operation. The biggest one in recent years in December 2017 (in one day) was $320 billion which is about 16 times the size of the repurchasing operation on 18th September.

The TED spread (the treasury euro dollar spread) is currently 21 basis points, that's lower than the long-term median of 40 basis points. This means there's plenty of money in the US banking system. The investment grade corporate bond spread (the BAA spread) which we look at in our quarterly is trading at 217 basis points and that's lower than long term median of 220 basis points. There's plenty of money in the US banking system and the US corporate debt market.

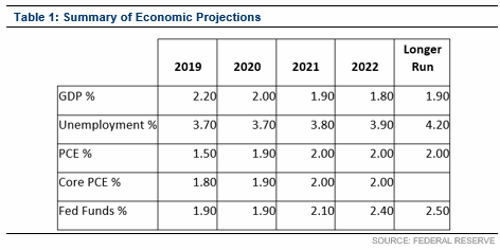

The View from the Fed

The Summary of Economic Projections released by the Fed after its September meeting is shown as Table 1. The Fed changed its views in its outlook for the US economy to become moderately optimistic. They increased their outlook for GDP growth this year from 2.1% to 2.2%. They think that growth next year will be 2% in 2020, 1.9% in 2021 and 1.8% in 2022.

The result of that is that they think that unemployment in the US is bottoming out now at 3.7% and it will be 3.7% next year rising to 3.8% in 2021 and 3.9% in 2022, in the long run unemployment rises to 4.2%.

Due to slightly better growth, the US gets slightly higher inflation. PCE (personal Consumption Expenditure) inflation is 1.5% this year. It is expected to rise to 1.9% next year and 2% the year after that. Then PCE inflation should stay basically at 2% forever. This is central bank nirvana because that's where the Fed target is.

Advertisement

As a result, the Fed thought that they had finished cutting the Fed funds rate. The effective Fed funds rate after last week's cut is at 1.9%. The Fed thinks they will leave it right where it is at 1.9% next year, and the year after that it's going to go up to 2.1%, then to 2.21% in 2022. In the long term they expect a Fed funds rate of 2.5%.

The Fed is wrong. The reason the Fed is wrong is because the US economy is going to be significantly weaker than their estimate of 1.9% in 2021. We know from our analysis of the shape of the yield curve that in 2021 the US will be in a soft landing or growth recession. A soft landing doesn't mean that you have just a 10 basis point drop in growth. A soft landing will feel like a recession but growth in GDP terms will still be positive. Unemployment will be going up much more rapidly than the Fed thinks.

As a result of the Fed being wrong about growth in 2021, they're wrong about where the Fed funds rate is going to go for the next four years. They will realise as they get into the end of next year, perhaps earlier, that they need to cut rates further.

Our Fed funds rate model says that they'll need to cut at least one more time in the very near future down to 150 basis points. We think there'll be a lot more signals for further rate cuts. It's really great that the Fed is optimistic. It's really great that they think all of their troubles are over. Their troubles are not over.

As we move into 2020 and 2021, the actual movement in the US economy will be infinitely more entertaining than the US Federal Reserve currently believes.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

3 posts so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon