In June 2010, I was standing in Tiananmen Square looking towards the Great Hall of the People. Away to my right, in front of the Forbidden City, was a 12 square foot painting of Chairman Mao. It occurred to me that, even though we think that China has become a capitalist country and a capitalist economy, they are very much a communist country and a communist economy.

In the English-speaking world, economics is now based on the work of Maynard Keynes. In a communist economy, economics is based on the work of Marx and the work of Lenin. China is run by the Chinese Communist Party (CCP). The leaders of the CCP have learnt their economics from reading Marx and from reading Lenin.

Marx and Lenin are two parts of an economic history. This is an economic history of the development of the British economy in the 19th and early 20th centuries. The industrialisation of the British economy, and its progress between 1780 and 1860, is contained in the works of Karl Marx.

Advertisement

Marx emphasised commodities trading. He said that "a commodity, no matter how dirty or filthy, will make money of itself." As well as commodities, Marx also believed in the bond market. He talked about the "sovereignty of the bond holder". When you own the bond of another country, that puts you in a situation of power over that other country. Marx had a very high belief in gold. He said that "gold is the money of the world".

In the Chinese economy, there is a different emphasis on each of those things: commodities, the bond market and gold, compared to a Western economy. In a Western economy, we follow Maynard Keynes. He said that gold is a "barbarous relic". In China, representatives of the Central Bank of China encourage people to own gold.

Understanding the Marxist thinking of Chinese communist leadership allows us to understand why China is an essentially commodities orientated country and also allowed me to understand why China had built up its gold reserves. It has also built up reserves in the bonds of foreign countries and built up an emphasis on trading commodities.

Lenin wrote a book called "Imperialism: The Last Stage of Capitalism". He wrote it during the Great War when he was sitting in Switzerland, being paid by the Germans, and was about to start the Russian revolution. This book is an economic history of the late British empire, from a period of about 1860 to about 1910. It is based on the work of English economic historian J A Hobson.

Hobson talked about how, in the late British empire, Britain spread it's colonial influence not by moving armies or navies around the world, but by investment, and particularly, by investment in building ports and railways. He said that by building these ports and railways, Britain gained strategic influence in these particular regions. More importantly, it gained a service income from providing those ports and railways, and they gained additional exposure to resources in the hinterland of those places.

Advertisement

China has moved from a situation where it's basically a manufacturing economy to being predominantly a service economy, but it's still in a situation where the majority of their export revenue is gained by exporting manufactured products. This is why they have moved to find a source of services income by building ports and railways in other countries. That program is called Belt and Road.

But what China has attempted to do, to support this program, is to make the RMB a reserve currency. This is because Britain, in this period of economic expansion and imperial expansion in the late 19th century, made the pound Sterling the premier reserve currency of the world. China seems to have forgotten that in order to make that possible, Britain had already created important institutions, which China seems to lack. The first of these was an internationally respected central bank. The Bank of England had existed for almost 200 years. It was the faith in the Bank of England which generated international faith in the pound Sterling. Britain had also created an international banking network, to provide services to support trade financed in the pound Sterling.

China has none of these institutions. It doesn't have an internationally respected Central Bank, and it hasn't built an international network of banks and banking support services. What it has tried to do is go through official channels. Through the IMF, it's had the RMB included in the basket of currencies used by the IMF, called the Special Drawing Right (SDR). In addition, it has provided through the IMF, a series of currency swaps in which it has swapped the RMB with the currencies of other central banks, that are part of the SDR. As a result, it has built up its international reserves and the proportion of international reserves that are in RMB. Still, they were doing this from an incredibly low base.

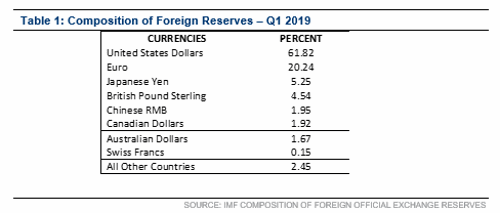

Even as short a time ago as the 2nd quarter of 2017, the RMB was only 1.07% of international reserves. This was a lower number than the Australian dollar had at that time. Table 1 shows us in the most recent time period, which is the first quarter of 2019, we see that the total proportion of international reserves held in RMB is still only 1.95% of total reserves. This is only slightly higher than the proportion held in CAD of 1.92% and the proportion held in AUD of 1.67%.

Even though China has been attempting to build up the RMB as a reserve currency, the proportion of international currency in RMB is less than half of the Pound Sterling at 4.54%, or the Japanese Yen at 5.25%. It is around about a tenth of the proportion held as Euros, which is 20.24%. The proportion of international reserves held in RMB is vastly lower than the overwhelmingly dominant international currency, the US dollar: 61.8% of all international reserves are held in the US dollar. In spite of all its efforts, the RMB is only a minor player in international reserves and international finance.

Trade War?

What happens when you have an international confrontation over trade between the US and China? What's supposed to happen, theoretically, is if a country puts up its tariffs relative to that of another country, that puts up its terms of trade. That means its exchange

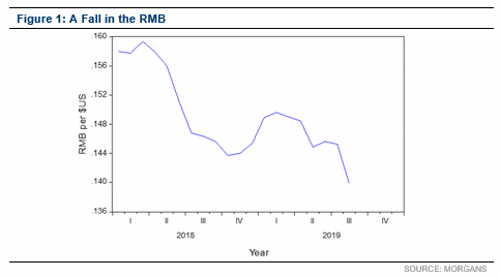

rate goes up against the country, on which its increased tariffs. Back in March 2018, Donald J Trump, President of the US first increased the tariffs on imports of Chinese goods into the US. The USD should have started to go up, and the Chinese RMB should have started to go down. That's exactly what happened.

The RMB $US exchange rate is shown in Figure 1. The RMB peaks, relative to the USD in February 2018, immediately before the US starts to put up tariffs on imports of Chinese goods into the US. The RMB has been on average falling ever since. And as it falls, international reserves and international trade finance, which is held in RMB, is being sold and used to buy US treasury bonds.

Up until March 2018, our model of US bond yields was going up, based on the rise in the US Fed funds rate. Since the capital flight from China into US treasuries began in March 2018, we have seen an unanticipated but major decline in US treasury bond yields. This decline is shown in Figure 2.

That decline in US treasury bond yields (since the US 10 Year bond is the benchmark bond of the world) has led to a decline in all the bond yields in all of the countries which have advanced economies. We have seen a dramatic decline in Australian 10 Year bond yields, down to an all-time record low yield. This has happened just slightly after, but a direct result of, the decline in US treasury yields.

Our bond models, based on normal market conditions, tell us that we now have a situation where Australian 10 Year bond yields are 2.4 standard errors below where they should be in terms of yield, and US 10 Year bond yields are 2.7 standard errors below where they should be in terms of yield. This means that US 10 Year bonds, for example, are in an area where they are a little over the top one percent of possible valuations, as a matter of fact, Australian 10 Year bonds are the same.

Conclusion

These very low levels of bond yields have been caused as a result of the capital flight from RMB securities into US bonds as a result of the fear engendered by the trade war.

The major effects of the trade war seem not to be on trade but on financial confidence. Loss of financial confidence in the RMB is generating a flight out of RMB securities into US bonds. This has driven down the level of US bond yields.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon