On Wednesday 6 March, the Australian Bureau of Statistics released the Australian GDP numbers for the December quarter of 2018. These accounts showed year on year growth rate of GDP in trend terms as 2.3%. They also showed GDP growth in seasonally adjusted terms of 2.3%. In any other developed economy, these would be regarded as good numbers.

Nevertheless, some commentators have suggested that Australia is in a “per capita recession”. This is because in seasonally adjusted terms, GDP per capita fell slightly in the September quarter and the December quarter. This did not happen in the more reliable trend measure of GDP. In this measure, GDP per capita rose in the September quarter, but fell in the December quarter (see footnote).

Right there, we can see the two negative quarters of GDP in both the September and the December quarters are probably just because the seasonally adjusted numbers have more random variation in them, than the more reliable trend measures.

Advertisement

What we want to discuss here though, is the broader issue of how to interpret the Australian GDP numbers. The real GDP numbers published by the ABS are regularly taken to be an accurate estimate of what is happening in the Australian economy.

The problem for most of us is that they have almost nothing to do with the economy as we experience it. These real GDP numbers frequently tell us that the economy is in good shape, when everything around us tells us that it is rotten. These numbers may also tell us that the economy is in bad shape, when everything around us tells us, that it is really good.

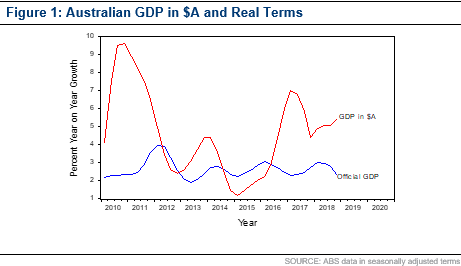

How does this happen? We can begin our investigation by looking at the chart below. Here we see the year on year rate of change of Australian GDP, in Australian dollar terms. We also see the year on year rate of change of Australian GDP, in terms of the real GDP numbers published by the ABS. For most of us, the economy that we experience is not the economy “in real terms”. The economy that we experience is the economy in Australian dollar terms. When we are paid, we are paid in Australian dollars. When we pay taxes, we pay taxes in Australian dollars. When the government receives tax revenue, it receives it in Australian dollars. When Australian companies make profits, those profits are published in Australian dollars.

In Figure 1 above, we can see why the growth rate of the Australian economy has appeared to the ordinary citizen to swing around so much since the beginning of this decade. Back when were still in the commodity boom in 2010, GDP in Australian dollar terms rose rapidly, but the GDP in real terms, as published by the ABS told us that the Australian economy was pretty much the same as it is right now. GDP growth in real terms was 2.34% for the year to Q4 2010 when there was a boom and 2.27% for the year to Q4 2018 when the economy is what it is today.

The difference may have been that in the year to Q4 2010, nominal GDP growth or GDP growth in Australian dollar terms, rose by 9.64%. On the other hand, for the year to Q4 2018, nominal GDP growth or growth in Australian dollar terms, rose by 5.5%.

Advertisement

Another time, when real GDP as published by the ABS as the same as now, was the year to Q4 2014. Back then, real GDP was published at 2.36%. This was almost the exact same number as in Q4 2010 and Q4 2018. Yet the Australian economy at that time was absolutely rotten. Wages growth had fallen dramatically and unemployment had gone up sharply. At that time, for the year to Q4 2014, nominal GDP growth was only 1.5%. It fell to 1.2% for the year to Q1 2015.

What this tells us, is that nominal GDP, or GDP in Australian dollar terms, tells us much more about how we actually experience the economy, than GDP “in real terms”, as published by the ABS.

Why is the ABS real number so misleading?

The problem with the lack of ordinary utility in the ABS number for real GDP, lies in the way the GDP deflator is calculated, and how it is used in the Australian context. Back in the 1980s, Australia became part of an international convention to move from the National Accounts done as Gross National Product, or GNP to Gross Domestic Product, or GDP.

The National Accounts for the GDP under the GDP system, were really designed for European economies exporting manufactured products. These products were subject to only modest price variation from year to year. Hence it made sense that when you wanted to calculate the contribution of those exports to a European economy in real terms, then what you would do, is you would divide the total income you got from selling those products, by the price of them. This gave you a reasonably stable understanding of the contribution of exports, to a small European economy.

The problem, is when you come to a medium sized commodity exporting economy like Canada or like Australia, this process generates a distortion which pretty much destroys much of the point of doing the National Accounts in the first place. Much of the information that would exist about the economy, is distorted by using this type of price adjustment.

The ABS publication of Wednesday 6 March tells us that GDP for the year to Q4 2018 in A$ terms went up 5.5% (seasonally adjusted). It also tells us, that after the GDP deflator is applied to the data, that GDP for the year to Q4 2018, in real terms, went up by 2.3%. The difference between these is 3.2%. What we are seeing here, is the size of the GDP deflator. What is interesting about this is that CPI inflation for the year to Q4 2018, which was also published by the ABS only increased by 1.8%. It is possible that ordinary Australians experience inflation at the rate, as described by the CPI. It is much harder to believe that ordinary Australians experience inflation at the rate described by the GDP deflator.

What happened in 2018?

What was actually happening in the Australian economy in the last two quarters in 2018, is that the improvement in the Australian economy was masked by a rapidly rising GDP deflator. Rising commodity prices led to a GDP deflator that was rising more rapidly than the CPI. This meant that the increase in output was divided by an increase in prices, which were much higher than ordinary Australians were experiencing.

What was happening to the Australian economy in Australian dollar terms is a much better description of what was happening, than the real GDP numbers published by the ABS. The real GDP numbers made the economy look much worse than it actually felt at the time.

When we reduce these lower growth numbers by quarterly population growth numbers, the end result is numbers that are lower still. The estimated population growth in Australia in 2018, was 1.6% per annum. This is the highest population growth rate of any developed economy. The reason that Australia has the highest population growth rate of any developed economy, is because Australia has the highest immigration rate of any developed economy. A 1.6% annual growth rate becomes a 0.4% quarterly growth rate. This means to calculate per capita growth rate, you must reduce the quarterly GDP growth number by 0.4%. This is how we got to such low growth numbers in Q3 2018 and Q4 2018.

Rising commodity prices meant that the increase in Australian dollar GDP, was divided by a number, which rose more rapidly than CPI. This made the economy look weaker than it actually was. These numbers were further reduced by quarterly population growth numbers.

GDP per capita recessions and other children’s stories

In the more reliable trend terms, GDP per capita only fell by one quarter last year, and that was the December quarter. This means that the idea of a genuine per capita GDP recession simply does not cut it. This does not mean that there has not been previous GDP per capita recessions in the past three decades. In fact, we find there are four such recessions. The first and the largest of these recessions was the Keating recession of 1990 and 1991. This was the longest per capita GDP recession, lasting a period of eight quarters.

The second such recession followed the crash in US technology stocks in 1999 and 2000. Australia experienced a per capita GDP recession beginning in Q3 2000 and ending in Q1 2001. This was the next longest per capita GDP recession and lasted three quarters.

There are two more such recessions. The next was in Q1 2006 and Q2 2006. This was a shorter period of only two quarters when per capita GDP in trend terms fell in each quarter. The fourth such event happened in 2008. There was a GDP per capita decline in Q3 2008 and Q4 2008 (don’t tell Kevin but it looks like we really did have a GDP per capita recession during his term as Prime Minister).

Conclusion

The Australian per capita GDP recession in 2018 is a figment of how the GDP deflator distorts the effect of export prices on the real Australian economy. In actual fact, the economy in 2018 was doing just fine. Improving commodity prices meant that Australian dollar GDP was growing at 5.5% in seasonally adjusted terms. This rapid growth of the economy, in Australian dollar terms, explains why wages were just beginning to pick up and why Australian government tax receipts were improving at a much better rate that the government itself anticipated.

Per capita GDP recessions may actually exist. Describing 2018 as a per capita GDP recession, is just a story to scare children.

This article was first published by Morgans.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual’s relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“Morgans”) do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon