In his book "Can it happen again?" the late Hyman Minsky argued that western economies were subject to regular financial crises. These crises were the result of multi-decade periods of increasing debt relative to GDP followed by multi-decade periods of decreasing debt relative to GDP.

Minsky argued that debt would rise relative to GDP until the total interest payments relative to GDP would consume too high a level of national income. The peak in debt would lead to a sharp lift in savings. This increase in savings and fall in consumption was often experienced as a crisis. From this point, the growth in debt would come to an end and savings would sharply rise. This rise in savings and fall in consumption would lead to a long term period of falling debt relative to GDP.

Advertisement

Minsky was talking about cycles in private debt. The transition from rising debt to falling debt has been called by some commentators "a Minsky moment". These commentators tended to refer to the global financial crisis as just such a "moment".

Hyman Minsky died in 1996. The two best commentators on the historical process of financial crises currently living are Kenneth Rogoff and Carmen Reinhart. Together, they have published the most authoritative works this century on the history of the transition to and the transition from major financial crisis.

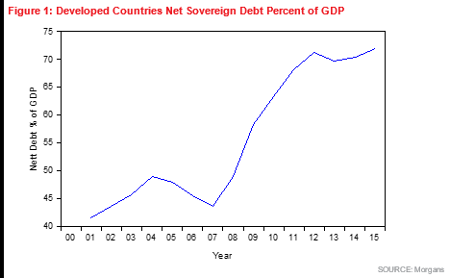

Rogoff and Reinhart note that one of the distinguishing features of the global financial crisis is that the world has emerged from it with extremely high levels of public debt. In Figure 1 above we show the level of net sovereign debt as a

percent of GDP owed by developed economies. The data for this series is published in the International Monetary Fund International Outlook database. We can see that the level of net debt owed by developed economies rises from 43.6% of GDP in 2007 to 71.3% of GDP in 2012. This is a rise of 27.7% of GDP in only five years. Our objective in this paper is to examine the effect of this high level of developed country net debt upon financial markets and ask the question as to how this high level of developed country debt may be paid back.

When has this happened before?

The precedent for the repayment of high levels of public debt can be found by examining the repayments of large levels of war debt by allied countries after World War II. The United States, the United Kingdom and Australia, all built up very high levels of sovereign debt in World War II. This was successfully paid back over the period from 1946 to 1980. How was this done? What can we learn from this?

Advertisement

Carmen Reinhart has done work in this area with a number of other collaborators. One of her papers on this issue is aptly called "The Liquidation of Government Debt". She wrote this in 2011 with Belen Sbrancia. I attended her presentation of this paper at the American Economic Association annual meeting in Chicago in 2012. In this paper she talks about "financial repression".

Reinhart says that financial repression usually includes long periods where the interest on government bonds is persistently below the rate of inflation. She says that this allows the reduction in sovereign debt relative to GDP to continue over a long period of time without giving rise to political disorder. She says "given that deficit reduction usually involves highly unpopular expenditure reductions and/or tax increases in one form or another, the relatively stealthier financial repression tax may be a more politically palatable alternative to authorities faced with the need to reduce outstanding debts".

Reinhart tells us that the major way of repaying this debt after World War II was to run extended periods where the nominal interest rate on the debt was below the inflation rate that year. This is what we call 'negative real interest rates'. The numbers for Australia published in her paper are most insightful.

She examines the period from 1945 to 1968. She tells us that during that period the real interest rate on Australian bonds was below 3% in 92.3% of the years. She tells us that the real interest rate on Australian bonds as below 2% in 80.8% of the years. She tells us that the real interest on Australian bonds was below 1% in 65.4% of the years. Most importantly she tells us that the real interest rate on Australian bonds was below zero percent in 48.0% of the years.

What this means is that in the post war period, real interest rates on bonds in Australia was so low that they were reducing the real level of public debt in 48% of the years. The holders of Australian bonds were losing money in real terms around one year in every two.

Reinhart notes that investors in UK and US bonds were doing not much better. Investors in UK bonds received a negative real return in 47.8% of the years. Investors in US bonds received negative real returns in 25% of years.

To reduce sovereign debt relative to GDP only requires that the real level of debt grows more slowly than the real level of GDP. As long as the budget is balanced, debt to GDP will fall by the growth rate of nominal GDP (real GDP plus inflation) minus the interest rate on sovereign debt.

She says that "for the United States and the United Kingdom, the annual liquidation of debt by negative interest rates amounted on average from 3% - 4% of GDP a year. Obviously, annual deficit reduction of 3-4% of GDP quickly accumulates (even without any compounding) to a 30% - 40% of GDP deficit reduction in the course of a decade. For Australia and Italy, which recorded higher inflation rates, the liquidation effect was larger (around 5% per annum)."

Are we facing a new period of financial repression?

In Figure 2 below, we see the relationship between the real yields on US 10 year bonds and the level of net sovereign debt as a percentage of GDP in the developed countries shown in Figure 1. A model of the relationship between these two variables tells us that each 1% increase in net sovereign debt in developed economies will reduce the equilibrium yield on US 10 year bonds by 6 basis points. The T statistic of this relationship is 13.7. This means that the probability of this being a chance relationship is less than 1 chance in 10,000.

We can see that the relationship exists. The US 10 year bond is the benchmark bond of all world bonds. A lower real yield on the US 10 year bond means that all real bond yields will be lower. The result is that the higher level of sovereign debt in developed countries gives us a lower level of real bond yields in all developed countries (all other things being equal).

As long as this level of sovereign debt is high, we will have an extended period of lower real bond yields. This will have the positive benefit of allowing the repayment of this sovereign debt over an extended period as it did after World War II.

Why is this happening?

Let us go back and look at the world of Minsky. Minsky told us that when debt rises relative to GDP, interest payments consume a higher proportion of national income. The result is an enforced increase in savings. When savings increases, consumption falls. So, the result of a high level of sovereign debt in developed countries means a lower level of demand or consumption in developed countries.

We all know what this feels like. Since the global financial crisis, the recovery in demand has been disappointing, growth has been slow and the low level of demand has generated lower inflation.

What is important is how Central Banks react. Central Banks have responded to the low level of demand and lower inflation by cutting interest rates. In many countries they have cut interest rates all the way down to zero. Official interest rates have been zero even though inflation has been positive. This of course means that at least at the short end of the yield curve we have been re-entering the world of negative real interest rates. When this is maintained for many years, this reduces the level of sovereign debt at the short end of the yield curve. But wait, there's more.

The great innovation of Central Banks since the global financial crisis has been 'quantitative easing'. This means that Central Banks have been buying long term debt and reducing the yield on long term debt relative to inflation. This has reached the point in the Euro Area where as we speak, German 10 year bunds have fallen to a yield of 70 basis points. They were even lower than this earlier in the year.

Now for long term yields to be low enough to reduce net debt to GDP, they only have to be lower than nominal GDP for that year. We can rest assured that the combination of GDP growth in Germany plus even slight inflation will be higher than 70 basis points in 2015. This means that this market driven form of financial repression will be working to reduce German debt this year.

The same will be true of other European countries with even slightly higher interest rates on their long term debt. As long as countries can get a reasonable control of their budget deficits, this combination of low interest rates on long term debt plus modest inflation, will serve to reduce debt to GDP in the long term.

Conclusion

The data tells us is that we are living through the second great age of financial repression. The high level of public debt in developed economies and the reduction in income from servicing the interest rates on that public debt is reducing demand. Central Banks are responding to that fall in demand by giving us very low levels of interest rates.

We are facing an extended period of low real interest rates in the developed world. These low real interest rates will help to repay public debt. However, this process will take many years. The result will be an extended multi year period of low interest rates.

The information contained in this report is provided to you by Morgans Financial Limited as general advice only, and is made without consideration of an individual's relevant personal circumstances. Morgans Financial Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents ("Morgans") do not accept any liability for any loss or damage arising from or in connection with any action taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients of Morgans and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of Morgans. While this report is based on information from sources which Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect Morgans judgement at this date and are subject to change. Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon