Over recent weeks, commentators have repeatedly claimed Australia's high housing prices are due to a supply shortage. Former Treasurer Peter Costello blamed surging housing prices on a shortage, as did Alan Kohler. Treasurer Joe Hockey has a similar perspective, claiming:

It is just an infinite mantra for international commentators, for analysts based overseas to say 'well, you know, there's a bit of a housing bubble emerging in Australia'. That is rather a lazy analysis, because fundamentally we don't have enough supply to meet demand. That doesn't suggest there's a bubble; there might be a price increase of some substance, but you'd expect the market to react and produce some more housing.

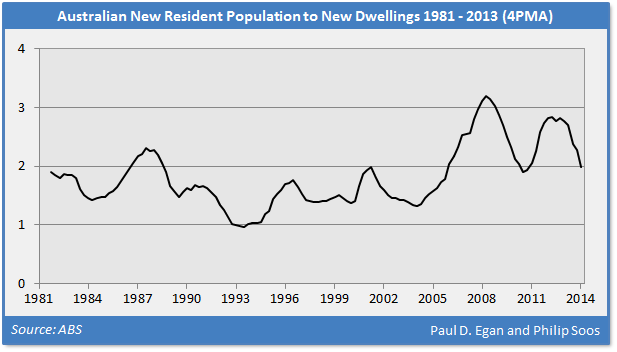

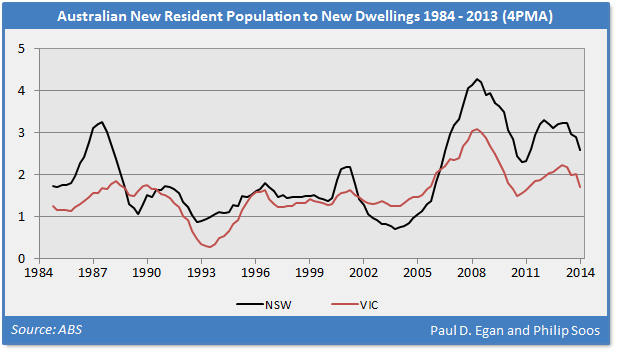

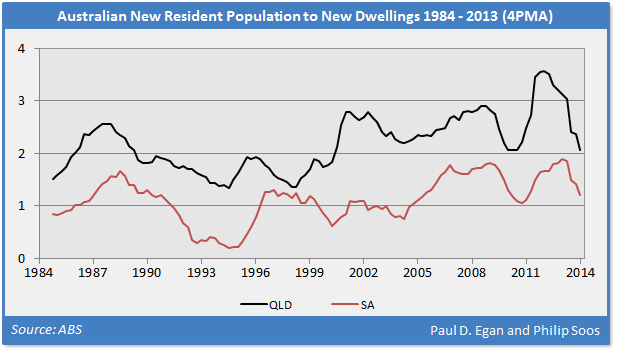

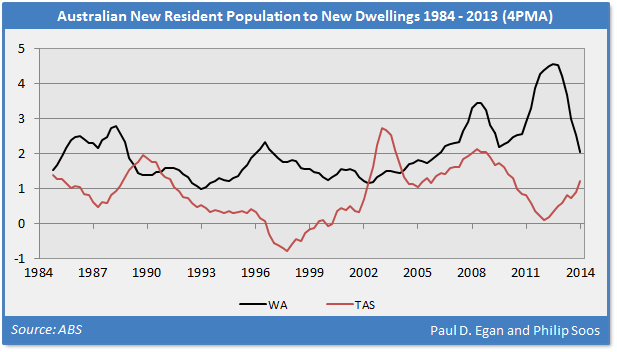

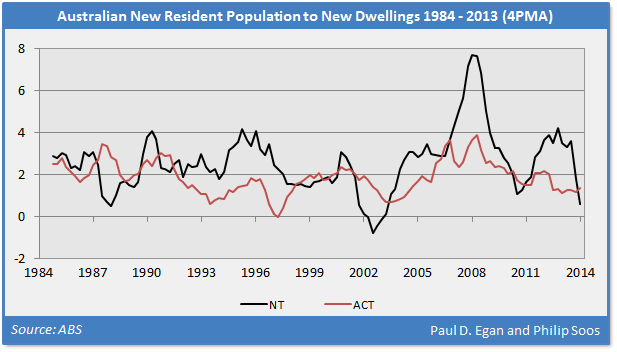

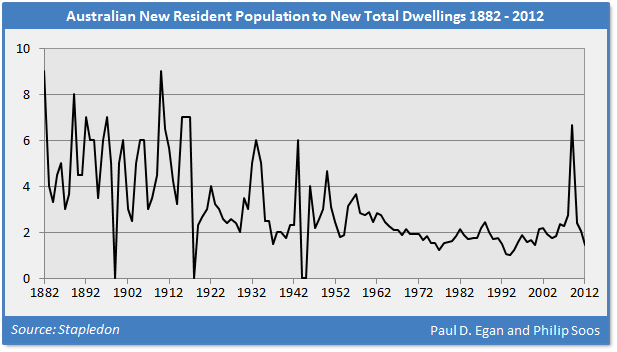

For over a decade, the common refrain is a shortage of dwellings has driven up housing prices. It is a mantra repeated endlessly by government, industry and academia. While it is easy for vested interests to claim a shortage exists, the data paints a different story. A good way to examine whether an adequate supply of housing exists is to compare the flow of new dwellings to new net population. Many analyses simply look at the relative or absolute change in dwelling stock, which is pointless without first considering changes in population.

Advertisement

Also, comparing the flow of new dwellings to existing population says little as new supply matters most to the net flow of new people, rather than the majority of the population who are already housed. It is important to note there are factors that are not captured in the ratio that require additional consideration:

- The total population measure is used, although only adults should be considered, for children don't purchase homes, make mortgage payments or pay rent.

- An increase in the natural population through births doesn't automatically necessitate new dwellings be built, though it may result in families upgrading to larger dwellings.

- Renovations and extensions of existing dwellings are overlooked, but generate additional housing capacity.

- Many immigrants arrive in groups, requiring only one dwelling per family/shared household.

- Building completions do not take into consideration dwellings that are demolished, condemned or held off the market.

- The slow rise in sole occupant households, divorce and/or childless couples (demographic change) may drive a long-run trend toward lower occupancy rates in general.

A total housing stock series adjusted for demolitions would be better than using housing completions, but there are no long-term housing stock series available for the states and territories on a quarterly basis. The series for building completions, however, provides a reasonable measure to illustrate general trends. Overall, the factors above probably have the net effect of understating supply. Due to the volatility of these data series, a 4-period moving average (4PMA) trend line is used to clarify the trends.

Advertisement

Discuss in our Forums

See what other readers are saying about this article!

Click here to read & post comments.

1 post so far.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon