Australia is once again proving itself to be the Land of the Tweedles. Though Labor and Liberal loudly proclaim their differences, on the key economic issues, they're (pardon the pun) carbon-copies. Both agree that the Federal Budget should be returned to surplus. Both believe that the "Global Financial Crisis" (which Americans and most of the rest of the OECD call "The Great Recession") is behind Australia, and the imperative now is to stop the growth in government debt. And both would leave untouched spending programs that make us worse-off by promoting asset bubbles rather than serious investment.

On their core economic beliefs, Tweedledee and Tweedledum are wrong. The GFC is still with us, and-certainly in Australia-government debt is not the key problem. Government policy that aims to drive the budget back to surplus may instead drive the economy back into recession.

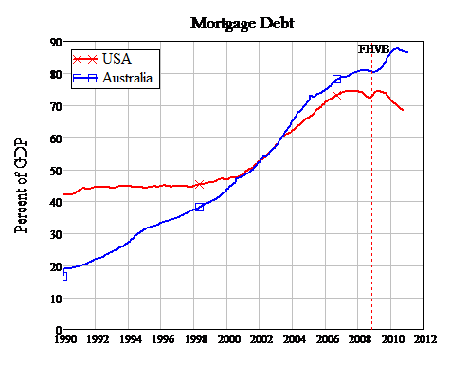

Though 'Dee and 'Dum raucously debate the level of government debt, both the boom before the GFC and the crisis after it were caused by out-of-control private debt. Rising household debt fuelled bubbles in asset markets-particularly housing-across the OECD. While Dee and Dum concur that Australia was a responsible exception to the global rule, the bubble in household debt here was in fact bigger than that in the USA-mortgage debt peaked at 74% of GDP in the USA in late 2007; Australian mortgage debt peaked 14% higher, at 88% of GDP, in March 2010.

Advertisement

Figure 1

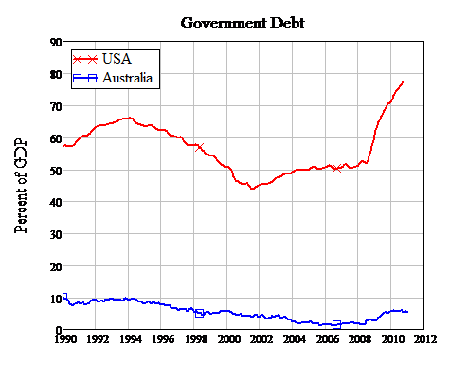

Against this, the level of government debt in Australia about which both Dee and Dum obsess is trivial. If government debt is a serious problem-an issue I return to later-then the USA might have something to debate. American government debt is 15 times larger than Australia's-relative to our respective GPDs. And American government debt is 117% the level of mortgage debt; while in Australia the ratio is less than 7%! That Dee and Dum can fill the airwaves with alarm about the level of government debt in Australia is truly surreal.

Figure 2

Dee and Dum concur that we avoided the GFC because of our lucky relationship with The Red Queen (China). There is some truth to this (they can't be consistently wrong), but both avoid discussing the major reason we boomed while the rest of the world slumped-which is that Dee encouraged households to keep on borrowing money while the rest of the world was deleveraging.

Advertisement

Dee and Dum don't discuss this policy-they call it the First Home Owners Scheme, I call it the First Home Vendors Scheme-because both worship the sacred cow of rising house prices. The twins both favour expensive affordable housing-yes I know that's a nonsense phrase, but we're on the other side of the Looking Glass here. So they both maintain, without discussion, policies designed to keep house prices high and ever rising, while at the same time pretending to make housing affordable with expensive policies that help keep the budget in deficit.

That's why, despite their obsession with reducing the deficit, neither Dee nor Dum will even discuss three simple policy ideas:

These policy changes would do wonders for the Budget bottom line while improving the economy-which both Dee and Dum claim they're trying to do ("Trust us, we're Tweedles...").

With roughly 100,000 First Home Buyers every year, 90% of whom buy an existing property rather than a new one, the abolition of this house price support scheme (that's not what Dee and Dum call it, but that's what it is) could save $600 million a year-and the continued support for new housing might spur housing construction as the Boost did in 2008. That's a rather more responsible way to save money than by cutting medical research funding, which is one of the deficit reduction kites Dee flew a month back.

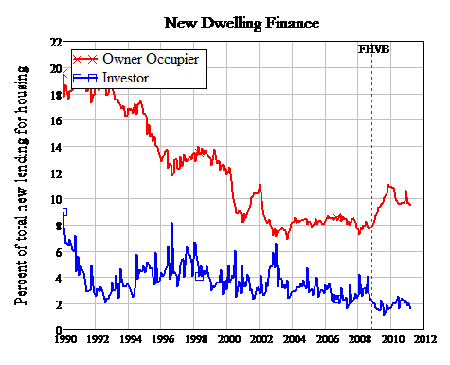

Limiting negative gearing to new properties only would also do something to increase the supply of new housing for renters. Both Dee and Dum claim that is the real goal of the current policy, but despite their bleatings, everybody knows that, as a scheme to encourage speculation on rising house prices, negative gearing is simply another plank in their mutual house price support scheme. So-called investors actually do less real investment than even owner-occupiers these days-less than 2 percent of new dwelling finance goes to investors building or buying new properties.

Figure 3

If negative gearing was restricted only to real investors-people who actually build something new, rather than buying something old and waiting for its price to rise-then renters might someday be able to find somewhere to rent.

Limiting negative gearing to new properties only wouldn't affect current property speculators (I'm sorry, I meant investors)-at least not directly-but it would reduce the growth of this Budget-sapping Black Hole by 95% or more.

Finally, the decision to halve the rate of capital gains tax back in 1999 was one of the stupidest things Dum ever did (when he was in power)-and therefore it worked a treat in Looking Glass Land. It costs the government close to $10 billion dollars a year-almost the amount of the deficit they're both claiming to know how to reduce. And, like everything else Dee and Dum don't bicker over, it promotes speculation over true investment.

Now it's the main cause of a blowout in the Budget deficit this year we're told, as capital gains have evaporated from our anaemic share market and the now bursting house price bubble. So why not make the Budget hit less extreme by bringing the rate back to the same as that for income?

Are either of them likely to even discuss abolishing this tax distortion? Not on your Nellie. And the same goes for the other two policies too, because behind their facade of debate, Dee and Dum both know that anything that would reduce house prices-and genuinely make them affordable-would lose them votes with the Looking Glass electorate. So even though these policy changes would probably eliminate the deficit overnight-which they both claim to want to do-they will instead fight about how hard to hit the soft targets of welfare recipients, universities and their own bureaucracy.

Which brings us to the other issue on which they both agree: the need to reduce the government deficit. Are they right?

In the interests of promoting healthy scepticism here, let me propose a simple rule of thumb: almost anything that Dee and Dum agree upon is likely to be wrong (and this applies in the USA as well to their Dee and Dum).

Firstly, government debt didn't blow out on its own accord: it grew because private debt stopped growing. This is obvious in the US data: government debt fell after the 1990s recession ended-and only rose since late 2001 because of foreign wars. Government spending blew out in 2008, not because the Dumocrats took over from the Deepublicans, as their political debate would have it, but because private debt-financed spending collapsed when the housing and stock market Ponzi Schemes ended.

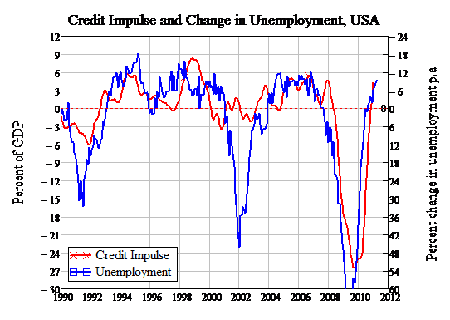

Figure 4

Secondly, it's a nonsense to argue, on an analogy with households, that government debt can bankrupt a government that has a captive Central Bank. If a household spends more than it earns, then after it exhausts its supply of credit, it is bankrupt. But if a government spends more than it taxes, it accumulates a debt to its Central Bank... which it can pay by borrowing from its Central Bank. Unlike a private bank, a Central Bank can't refuse to lend to its primary borrower.

So Federal Government in the USA or Australia won't go bankrupt-though their States could, as could the Eurozone countries of Europe. Hence, what should be discussed are the economic consequences of running a deficit: assuming instead that a government can run out of money is TweedleDumming down the problem.

I apologise for complicating the debate here-Tweedle-dumming a problem is much more catharthic-but the indications are that this is not the time to be reducing government spending in either the USA or Australia. The crisis was caused by accelerating debt-which gives the economy a boost-giving way to decelerating debt-which drives aggregate demand down. This is easily shown by graphing the acceleration of debt-the Credit Impulse-against changes in unemployment (the correlation coefficients in the next two charts are -0.77 and -0.75-extremely high correlations over such a long period with such variable economic conditions).

Figure 5

Though Australia certainly was assisted during the GFC by its sales of coal and iron ore to the Red Queen, the real reason that it "avoided" the GFC was that it restarted the private debt engine more rapidly than America did. The Credit Impulse stopped its plunge at -12 percent of GDP here, versus a peak negative of -26 percent in the USA. Australia also spent less time in the red on the Credit Impulse than the USA: 26 months versus 30.

Figure 6

Now both economies are recovering, not because the physical economies are in good shape-they're both very sick, except for Australia's minerals sector-but because the Credit Impulse has turned positive in both countries.

Figure 7

This, however, is not a sustainable path to recovery.

Firstly, borrowing money and gambling on rising asset prices is what got us into this crisis in the first place: relying on a recovery in private debt to get us out of this slump is like prescribing more cancer as a cure for cancer.

Secondly, it's highly unlikely that either country can sustain the acceleration in debt that is needed to keep the Credit Impulse positive, because if they did, then at some point falling debt would have to give way to rising debt once more. Call me crazy, but I just can't see that happening.

Figure 8

So what is likely to happen soon-and sooner for Australia than for America-is that the positive boost from the Credit Impulse will run out, and turn negative again. If, at the same time, the government's input turns negative courtesy of deficit reduction, then the recession will return.

Ultimately, the only way out of this crisis is to abolish the debt that caused it: debt that financed speculation on rising share and house prices rather than to finance genuine investment. As Michael Hudson puts it so simply, debts that can't be repaid, won't be repaid. At some stage-maybe ten years after the Great Recession began, we'll finally learn the truth of that eloquent aphorism, and tackle the real cause of this crisis.

But until then, we'll distract ourselves by watching the pointless debate between Tweedledum and Tweedledee.

-

Limit the First Home Vendors Grant to new housing only;

-

Limit new Negative Gearing to new housing only; and

-

Bring the capital gains tax rate back into alignment with the income tax rate.

reddit this

reddit this

Seed Newsvine

Seed Newsvine StumbleUpon

StumbleUpon